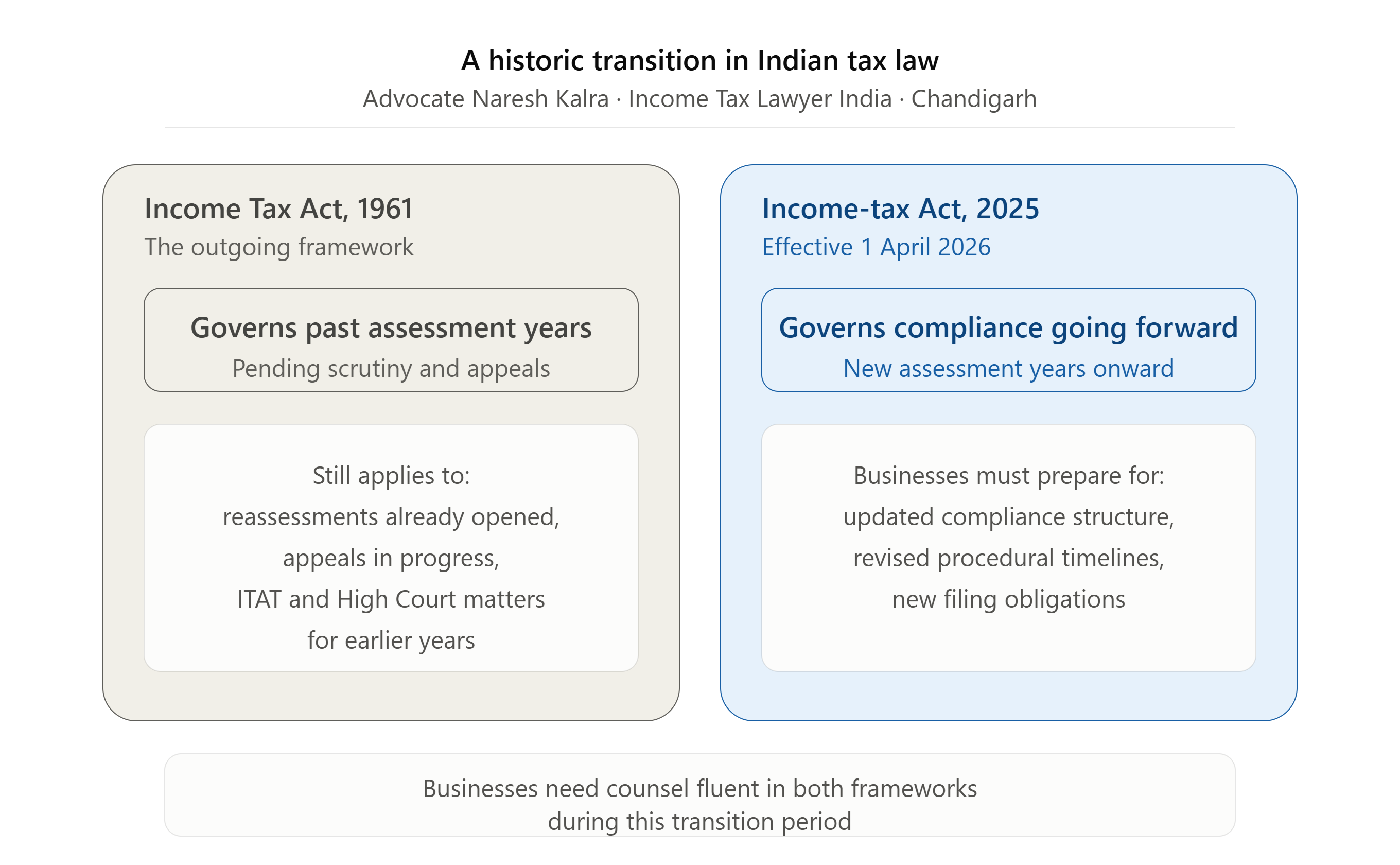

Income Tax Lawyer India — Protecting Your Business Through Every Assessment

India's income tax framework touches every major business decision — how you structure salaries, how you plan investments, and how you

respond when scrutiny arrives. A single error in return filing, a missed TDS deposit deadline, or an inadequately drafted response to a

notice can escalate into penalties and years of litigation. This is exactly why

businesses across Punjab need a genuinely capable Income Tax Lawyer India, not just an internal accounts team managing compliance reactively.

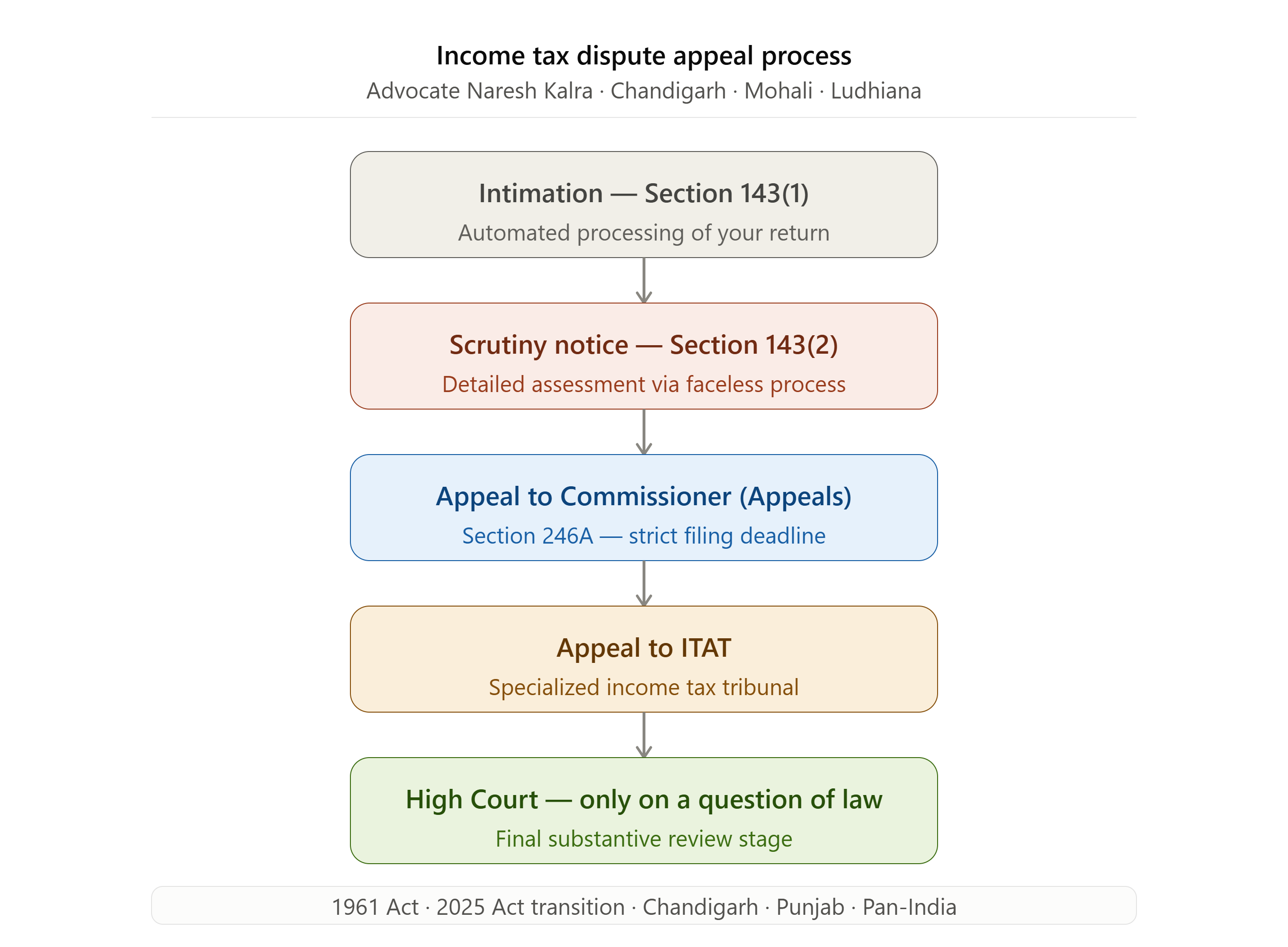

At the Law Offices of Advocate Naresh Kalra, we represent businesses, startups, and individuals in income tax compliance and

dispute matters across Chandigarh, Mohali, Ludhiana, and Pan-India. Our Income Tax Notice Lawyer India practice combines precise

statutory

knowledge with genuine understanding of how tax disputes actually affect business operations, cash flow, and long-term planning.